Why Some Garages Struggle to Get Insurance (or Pay More Than They Should)

Many Ontario garage owners discover that often at renewal or remarketing, their operation is not viewed as a “standard repair shop” by insurers. Certain activities, even when they seem minor or occasional, can push a business into a harder-to-place category, resulting in higher premiums, restricted coverage, or outright declinations.

7/10/20263 min read

Why Some Garages Struggle to Get Insurance (or Pay More Than They Should)

Many Ontario garage owners discover that often at renewal or remarketing, their operation is not viewed as a “standard repair shop” by insurers. Certain activities, even when they seem minor or occasional, can push a business into a harder-to-place category, resulting in higher premiums, restricted coverage, or outright declinations.

Below are five common red flags that can impact a garage’s insurability.

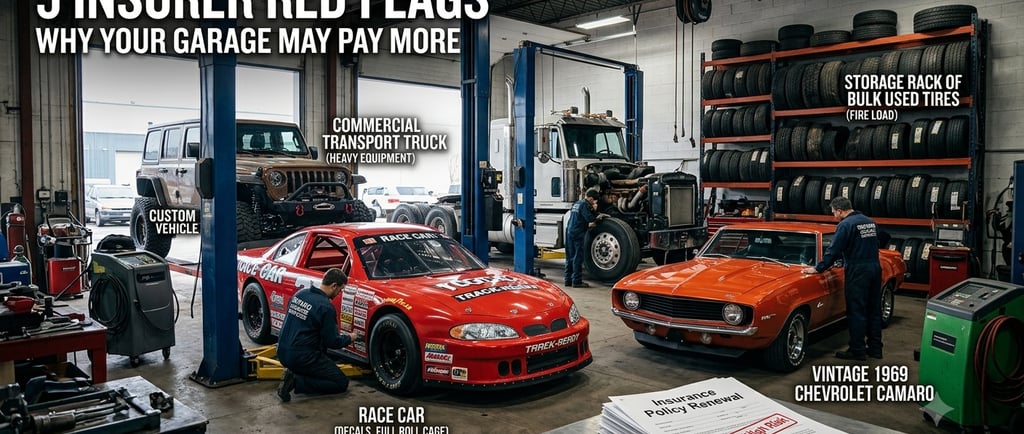

1. Race Car Work and Track Associations

Anything connected to racing tends to make insurers uneasy.

Even if a shop only occasionally works on track vehicles, visible ties, such as race car repairs, sponsorships, decals, or even marketing images, can signal higher risk. From an underwriting perspective, this raises concerns about performance exposure and liability if a failure occurs at high speeds.

Most standard policies exclude racing activities entirely, and many insurers will not quote garages that actively promote race-related work.

In one case, a garage owner had an old photo on his website showing him beside a race car in a race suit from years ago. The insurer flagged it and threatened non-renewal. After clarification and proper context, we were able to keep the policy in place, but it shows how closely insurers scrutinize perception, not just reality.

Many owners have personal ties to racing. The key is making sure it is clearly separated from the business.

2. Classic and Collector Car Repair

Working on classic or collector vehicles can be profitable, but it introduces complexity.

These vehicles often have:

Higher and less predictable values

Hard-to-source or irreplaceable parts

Greater sensitivity to cosmetic damage

A relatively minor issue can turn into a large claim, especially when originality or restoration quality is involved.

One of the biggest challenges is alignment between exposure and presentation. If a garage markets itself as a “classic car specialist,” insurers may assume a significant portion of the business involves high-value vehicles, even if that work only represents a very small percentage.

This mismatch can limit markets or drive pricing up.

A broker’s role here is to accurately position the risk. In many cases, classic work is occasional, and that distinction needs to be clearly communicated to underwriters.

3. Heavy Equipment and Non-Typical Vehicles

Expanding into heavier vehicles or equipment is common, but it is not automatically covered under a standard garage policy.

Servicing transport trucks, construction equipment, or specialty vehicles introduces:

Higher repair values

More complex mechanical exposures

Increased severity if something fails

Insurers will assess whether the operation has shifted from light auto repair into a more industrial profile.

There are also practical considerations, specialized tools, lifting equipment, and licensing requirements that signal a different class of risk.

If your operation evolves, your insurance needs to reflect that. Waiting until renewal (or worse, a claim) to disclose these changes can create serious coverage issues.

4. Vehicle Modifications and Custom Work

Custom work is one of the fastest ways for a garage to outgrow its policy.

Services like lift kits, performance tuning, structural modifications, and aftermarket installations introduce added liability. If a modification contributes to an accident, the garage can be pulled into a complex claim.

From a personal auto standpoint, most insurers will not cover vehicles that have been structurally modified. That concern carries over to the garage side as well.

Underwriters want clarity:

What types of modifications are being done

On what kinds of vehicles

Using which parts and processes

If a business promotes custom work but carries a basic “brakes and oil changes” policy, that disconnect can lead to restrictions or declination.

Reach out to the broker; modifications can be a difficult conversation, but a necessary one.

5. Tires, Bulk Storage, and Fire Load

Tires are often overlooked, but they represent a significant fire risk.

Large volumes of rubber, especially when stored improperly, can:

Increase fire intensity and spread

Complicate suppression efforts

Trigger stricter underwriting requirements

Insurers look closely at:

Storage methods and spacing

Proximity to buildings

Housekeeping practices

Fire protection systems

In some cases, standard water-based sprinkler systems may not be sufficient, depending on the volume, building construction and setup.

Poor storage practices can lead to higher premiums, added conditions, or refusal to insure altogether. Simple improvements, regular disposal, proper racking, and separation can make a meaningful difference.

Final Thought: Your Broker Should Be Part of Your Business

Garages are not “set it and forget it” risks.

Operations evolve quickly, new services, new equipment, new revenue streams—and those changes can directly impact insurance.

A good broker should be part of your advisory team, not just someone you hear from at renewal. A quick conversation before making operational changes can prevent costly surprises later.

In many cases, I recommend reviewing a garage risk at least twice a year. Things move fast in this space, and staying ahead of those changes is what keeps coverage intact and pricing competitive.

Disclaimer: This article is for general information purposes only and does not constitute legal, financial, or insurance advice. Insurance rules and coverage details can change, and individual circumstances vary significantly. For specific guidance about your policy, coverage options, or how these changes affect your situation, please contact a licensed insurance broker, agent, or insurer directly. You may also want to review the policy wording or consult with a legal professional for personalized advice.